Tweet

Tweet

Hello,

I am 28 and I run my own small company. I was always disciplined if it comes to money, especially when I was a student and had very little.

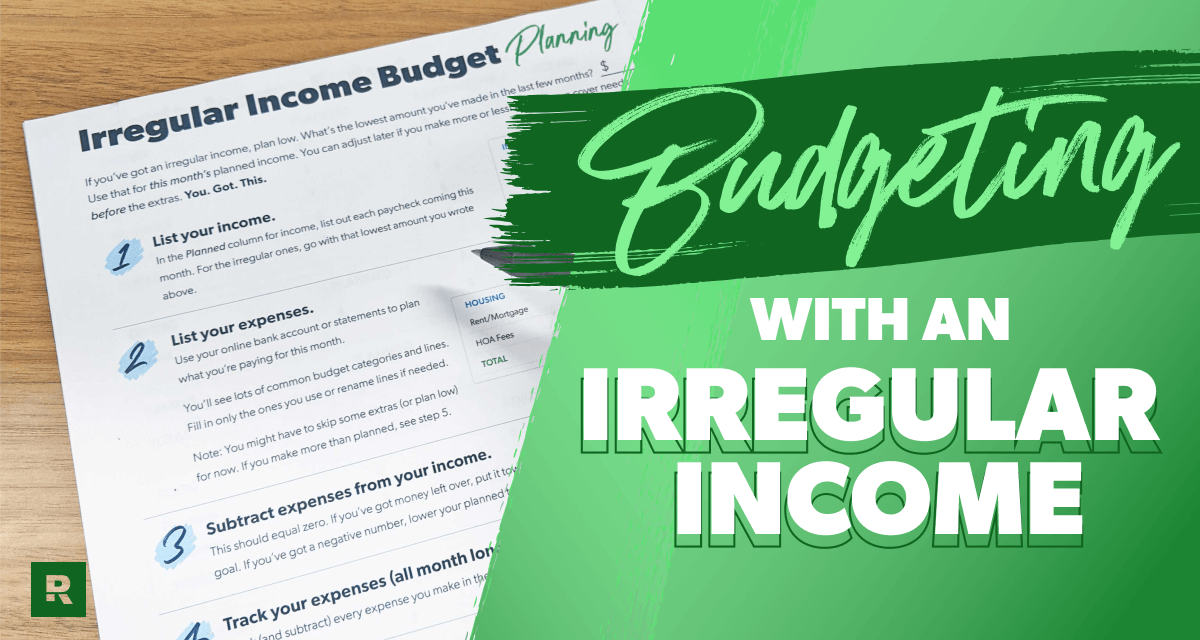

Recently, I realized that I spent a lot of. I have problems with estimating my real monthly income, because different clients pays me on different days. I am not able to tell how much I will earn next month. Sometimes, I don't realize that I have already spent the money that I was expecting to receive (when a client pays me earlier).

However, I have no debts (no loans, no credit cards, no mortgage).

I used to live really comfortable lifestyle, but I wouldn't say that it is exaggerated. I like eating out and pampering myself with quality wines, but I don't frequent expensive restaurants. I like shoping, but I rarely buy something that I don't need (I buy quality products that last years, I think twice before making a purchase - most of the time).

Still, after looking at my bank account I am often schocked and wonder where my money goes. I would like to change that.

I have around 10.000 euros in my saving account and around 3000 in my current account. I would like to learn how to save in a more efficient way, because I feel that I waste my money (and I would like to know where).

I am 28 and I run my own small company. I was always disciplined if it comes to money, especially when I was a student and had very little.

Recently, I realized that I spent a lot of. I have problems with estimating my real monthly income, because different clients pays me on different days. I am not able to tell how much I will earn next month. Sometimes, I don't realize that I have already spent the money that I was expecting to receive (when a client pays me earlier).

However, I have no debts (no loans, no credit cards, no mortgage).

I used to live really comfortable lifestyle, but I wouldn't say that it is exaggerated. I like eating out and pampering myself with quality wines, but I don't frequent expensive restaurants. I like shoping, but I rarely buy something that I don't need (I buy quality products that last years, I think twice before making a purchase - most of the time).

Still, after looking at my bank account I am often schocked and wonder where my money goes. I would like to change that.

I have around 10.000 euros in my saving account and around 3000 in my current account. I would like to learn how to save in a more efficient way, because I feel that I waste my money (and I would like to know where).

fun?

fun?

We can only get away with frivolous and dangerous lifestyles for so long.

We can only get away with frivolous and dangerous lifestyles for so long.

Comment